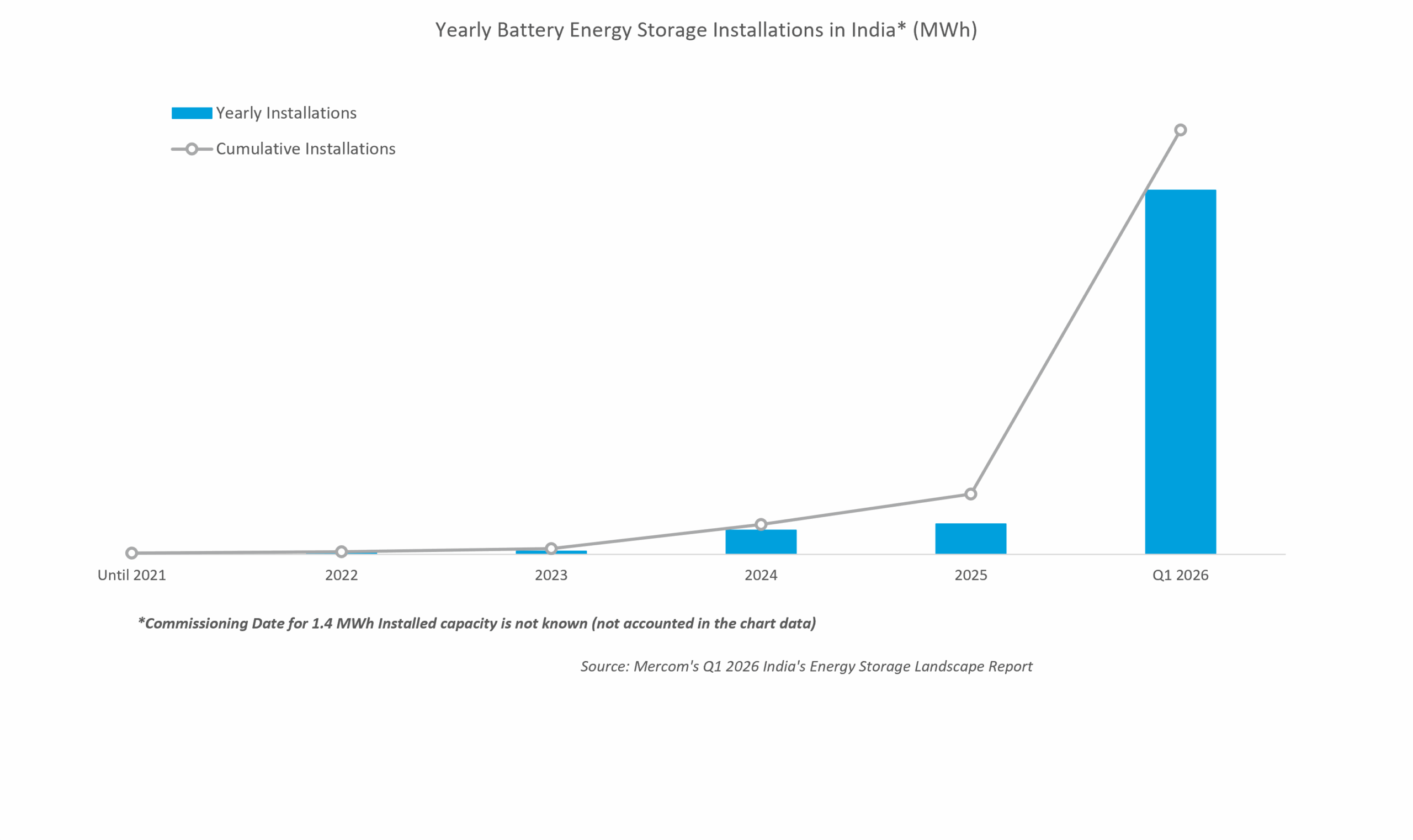

India Adds 4.6 GWh of Battery Energy Storage Capacity in Q1 2026

The cumulative installed battery storage capacity stood at 5.9 GWh

June 16, 2026

Follow Mercom India on WhatsApp for exclusive updates on clean energy news and insights

India added 4.6 GWh of battery energy storage capacity in the first quarter (Q1) of 2026, a 941% increase from 442.7 MWh added in Q4 2025, according to Mercom India Research’s Q1 2026 India’s Energy Storage Landscape Report.

The country’s cumulative installed battery energy storage capacity reached 5.9 GWh as of March 2026.

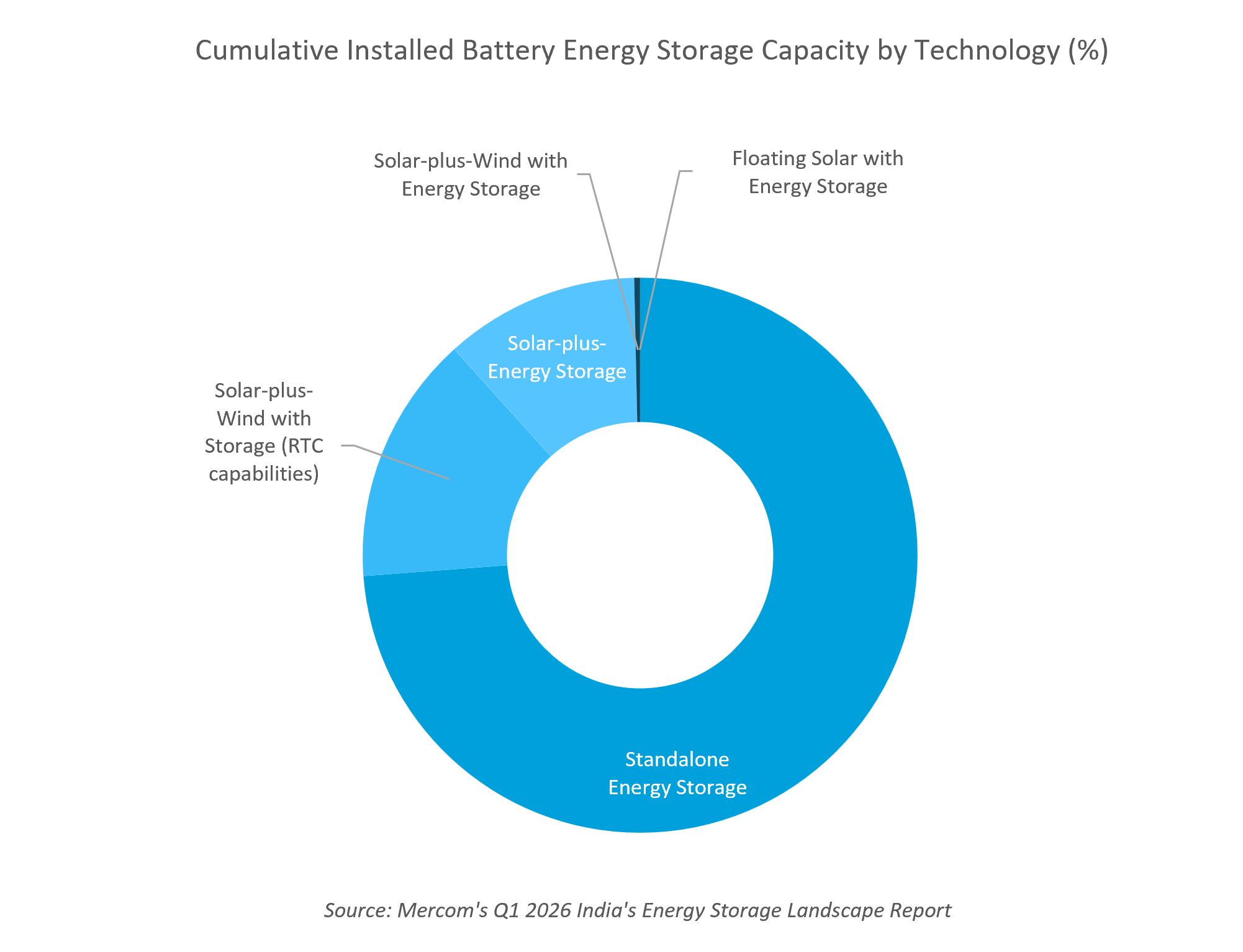

Standalone energy storage accounted for 73% of India’s cumulative installed capacity, followed by 15% from solar-plus-wind with storage (RTC capabilities) projects and 11% from solar-plus-energy storage projects. Other configurations, including solar-plus-wind with storage and floating solar with storage, contributed less than 1%.

“The energy storage sector is becoming an integral part of India’s power system as renewable energy capacity expands and grid management becomes more complex. Storage is no longer a future requirement; it is becoming central to maintaining grid reliability and flexibility,” said Priya Sanjay, Managing Director at Mercom India.

She added that the momentum behind storage is increasingly policy-driven.

“Energy storage is becoming increasingly important as renewable energy penetration grows. The government’s focus is on grid stability, and it recognizes that storage will be critical to achieving that. However, demand is not being driven only by the market. In many cases, restrictive policies and regulations are pushing commercial and industrial consumers toward battery storage,” Sanjay said.

The pumped storage project pipeline stood at 57.2 GW across projects in various stages of development. The installed pumped storage project capacity as of March 2026 stood at 7.2 GW, of which 5.7 GW was operational.

“The strong growth in Q1 2026, coupled with a rapidly expanding project pipeline, reflects how quickly energy storage is becoming a core part of India’s power infrastructure. Policy support, including the expansion of the VGF program and mandatory storage requirements for new solar projects, has accelerated market development and strengthened the sector’s long-term outlook. The next challenge is ensuring sustainable growth through realistic bidding, regulatory certainty, and policies that recognize storage as a strategic grid asset. As renewable energy penetration increases, storage will play a critical role in maintaining grid reliability and supporting the integration of large volumes of solar and wind,” said Raj Prabhu, CEO of Mercom Capital Group.

Rajasthan accounted for the largest share of cumulative installed energy storage capacity at 42%, followed by Gujarat with 25% and Maharashtra with 9%.

India’s energy storage development pipeline reached 69 GWh in Q1. This included 41 GWh of standalone storage, 11 GWh of solar-plus-wind with storage, 9 GWh of solar-plus-energy storage, and 1 GWh of solar-plus-wind projects with storage (RTC capabilities). Renewable energy-plus-storage projects with unspecified configurations of renewables and storage accounted for another 6 GWh.

Gujarat had the largest pipeline of standalone battery storage capacity at 10 GWh.

Multiple agencies issued tenders totaling 18 GW during the quarter and auctioned more than 4 GW of standalone storage projects.

Tender activity rose 47% from 12 GW in Q4 2025, while auction volumes declined 61% from 11.1 GW in Q4 2025.

However, the economics of battery storage continue to vary significantly depending on consumer load profiles, tariffs, and state-level regulations.

“Battery storage does not make economic sense for every consumer. The technology is most viable for C&I consumers with significant peak-period electricity consumption, particularly in states with steep peak-hour tariffs. However, for consumers whose demand profiles are not aligned with peak pricing, storage economics remain challenging, resulting in longer payback periods and lower returns on investment,” Sanjay said.

“In high-tariff markets such as Maharashtra, especially where peak-hour rates are elevated, battery storage can still make sense despite regulatory changes. But in states with lower electricity prices, similar restrictions could make storage economics unviable,” she said.

She added that DISCOMs and policymakers must balance grid requirements with market adoption. “There has to be a balance between encouraging adoption and imposing restrictions. If regulations become too restrictive, consumers will not install storage systems, and the objective of improving grid stability will not be met.”

The report noted that energy storage is gaining importance as India’s renewable energy capacity rises, requiring greater flexibility to manage variability and ensure grid reliability. However, storage deployment remains more complex than solar installations and requires greater technical and commercial expertise.

“Storage is not as straightforward as solar. A battery system cannot simply be installed and expected to deliver the same value across all applications. The industry is still understanding battery sizing, integration, optimization, thermal management, degradation costs, and long-term pricing structures. Wider market education is necessary for adoption to scale,” Sanjay said.

The need for a deeper understanding is greater in storage than it was in solar. Government agencies, DISCOMs, and the industry must work together to understand where storage works, how it should be deployed, and how policies can support adoption without undermining economics.

Mercom India’s Q1 2026 India’s Energy Storage Landscape Report spans 78 pages and provides a comprehensive analysis of all aspects of the country’s energy storage sector. It offers valuable insights into market dynamics, the policy framework driving capacity additions, and the overall trajectory of industry growth. For the complete report, visit: https://www.mercomindia.com/product/india-energy-storage-landscape-q1-2026

Arjun Joshi

More articles from Arjun Joshi.